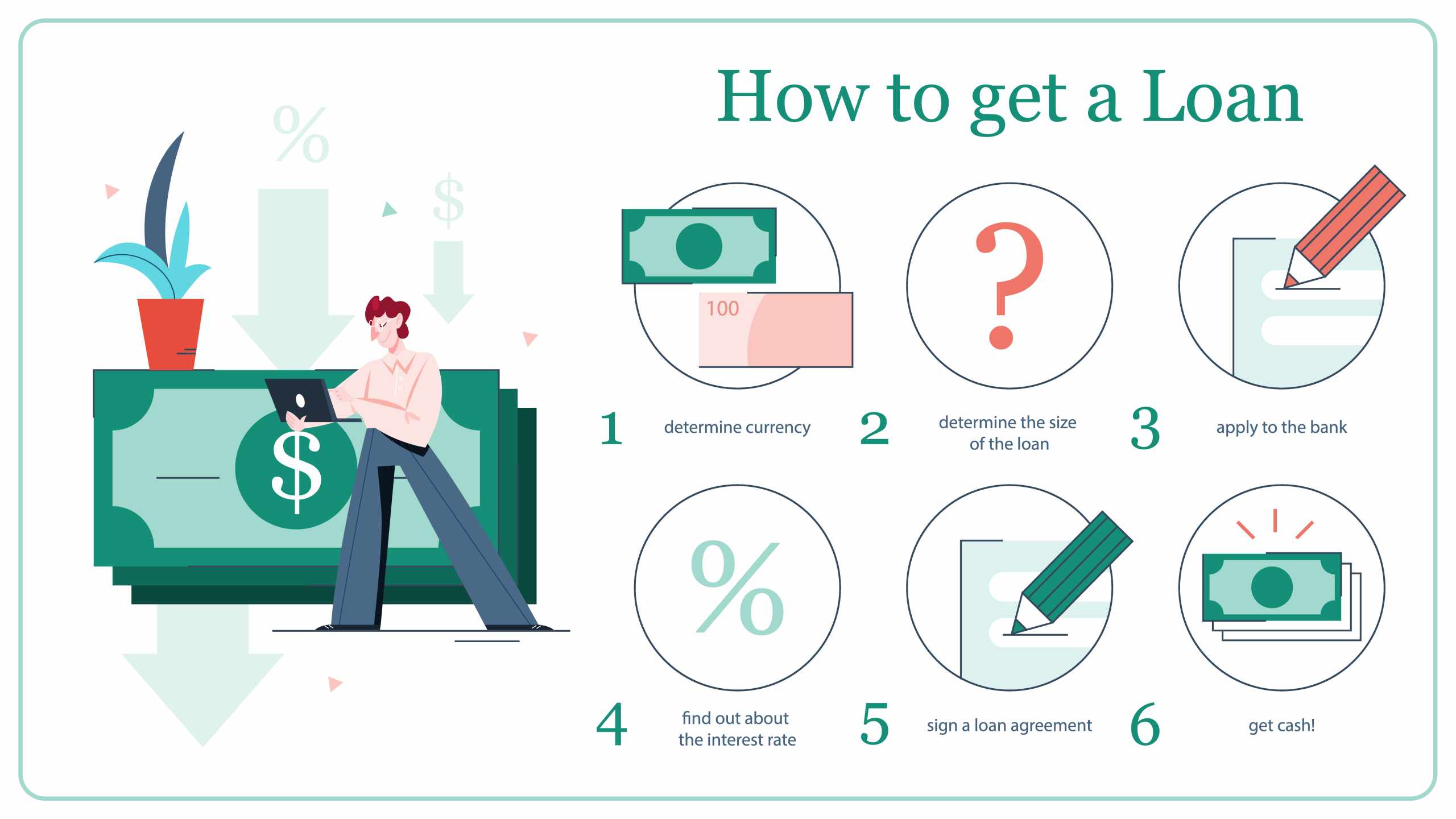

Home loans are availed mainly by applicants who wish to own a house of their own. The entire arrangement is a long-term process and is made available by the banks and NBFCs as per their business module. Home loans in the current market scenario are offered at a starting interest rate of around 6%. This ongoing market rate is productive and ensures your dream home at the lowest possible EMI rates. To sign yourself up for this commitment that extends to a long period, go through this list of home loan strategies to avail of a home loan without much hassle.

Table of Contents

Check on Your Credit Score

To get a home loan, one of the prerequisites is a healthy credit score or CIBIL score. A high credit score implies timely repayment of due bills, and a low credit score will mean that you are ineligible to pay your bills on time. The higher your credit score is, the lower your home loan interest rate on the amount will be. There are different ways in which you can improve your credit score. So if you feel like your score is not sufficient to get approved for a home loan, calculate and weigh your options to pay your bills properly. Try to clear your previous loans and then wait for some time to make your credit score sufficient to acquire a suitable home loan.

EMI Payment Capability

Before you opt for a home loan, calculate your repayment capability of the Equated Monthly Installments or EMI. Being well-versed about this will save you from financial burden in the long run. EMI calculation is something every home loan borrower should be aware of because a loan for a house is a long-term venture. You may be able to foresee your EMI payability for the upcoming five years. But a home loan repayment tenure extends for ten years or more, which means that there will be countless unprecedented events that may require immediate financial assistance. Calculate your savings beforehand and make sure that the home loan repayment gets done within time. Thus avoiding unnecessary financial burdens.

Monitor the Period for Loan Repayment

The loan repayment tenure plays an essential factor when it comes to borrowing a home loan. Normally, it is advisable to opt for a larger period because it eliminates the idea of a considerable amount to be paid every month. On the other hand, you can opt for a shorter period, but then the idea of paying a large amount of EMI may put unwanted pressure on savings, and by the time you finish off paying your home loan, you will be left with an empty savings account. To avoid that from happening, choose a period that is neither too long nor too short. That will sum up to a nominal EMI amount for you. But if you have a savings account with ample deposits saved up beforehand, you can always opt for a short period to pay the EMI in an immense amount every month and waive off the loan quickly.

A Large Amount of Down Payment

Down payment is a direct and one-time payment done by the applicant for obtaining a loan. It is also applicable for home loans. A large down payment will grant you a small loan amount which will lead to smaller amounts of EMI, and you can clear the loan along with its interest in a short period. This is applicable if you have ample savings previously. A large down payment means the chances of loan approval are very much higher, and the amount credited to you will be accountable and lessened of risk. But if you are not entirely fulfilled with previous savings, do not bother about a sizable down payment since this will only increase your monetary burdens. You should not get talked into acquiring a personal loan (or any other form of a loan) to abide by this down payment system. Just acquire funds for a minimum down payment and focus on building a formidable credit score.

To sum up all the points in this list, you must make sure to compare interest rates from bank to bank and get a possible deal to invest in for the home of your dreams. If you consider the factors explained above, you will indeed have a fool-proof and smooth experience acquiring a home loan for the first time without any hassles.